One of the biggest challenges in mobile banking is ensuring security without relying on extra hardware. Users often face systems that demand new SIMs, replacement cards, or specialized apps. These changes add cost and complexity, making adoption harder.

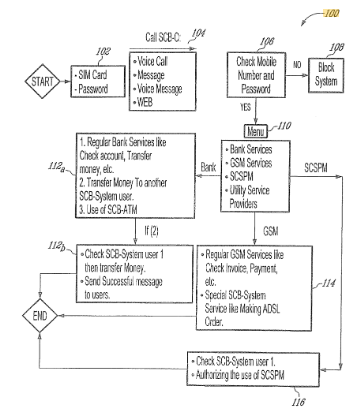

Patent US10032156B2 takes a different path. It shows how the SIM card already inside your phone can become the secure key for both telecom and financial services. A central operator validates the SIM and connects banks, networks, and service machines, enabling safe transactions in real time, without replacing hardware.

While the patent is part of a dispute between Delaware Horizon, Inc. and Central Bank of Oman, this article focuses on the technology itself.

Using the Global Patent Search (GPS) tool, we also explore related inventions. These reveal strategies like linking SIMs to payment cards, creating multi-purpose “super SIMs,” and using mobile-based PIN prompts to confirm payments.

Understanding Patent US10032156B2

US10032156B2 outlines a secure framework for enabling financial transactions through mobile devices. The system connects users, banks, telecom operators, and service machines via a centralized operator. This operator authenticates user identity through SIM credentials and facilitates direct, encrypted communication between all parties involved in a transaction.

Source: Google Patents

Its Four Key Features Are

1. No SIM replacement needed – Works with any existing SIM card or mobile device.

2. Operator-based authorization – A central operator routes transactions securely to the user’s bank.

3. User authentication via SIM identifier – Validates users by linking the SIM’s phone number to bank records.

4. Real-time financial requests – Enables secure, authenticated banking without storing sensitive data on the device.

Beyond these core features, the system supports multi-channel access via voice, SMS, or data. It allows users to connect to ATMs and service machines using only their mobile device and SIM. Each SIM can be granted different access levels, supporting flexible user control. Transactions between banks are verified through a dual-confirmation model, improving security. A risk monitoring layer actively detects and blocks suspicious activity across the network.

This invention presents a flexible, interoperable approach to mobile banking. It eliminates hardware dependency and simplifies user access across networks. The system is designed to scale across financial and telecom ecosystems.

Related Read: For a broader market context on banking integrations and digital wallet flows, explore our roundup of embedded finance startups.

Similar Patents As US10032156B2

To explore the technology space surrounding US10032156B2, we used the Global Patent Search tool to identify related inventions. These references deal with secure mobile transactions, SIM-based authentication, and remote financial operations. They reflect recurring themes in decentralized banking and telecom-integrated financial systems.

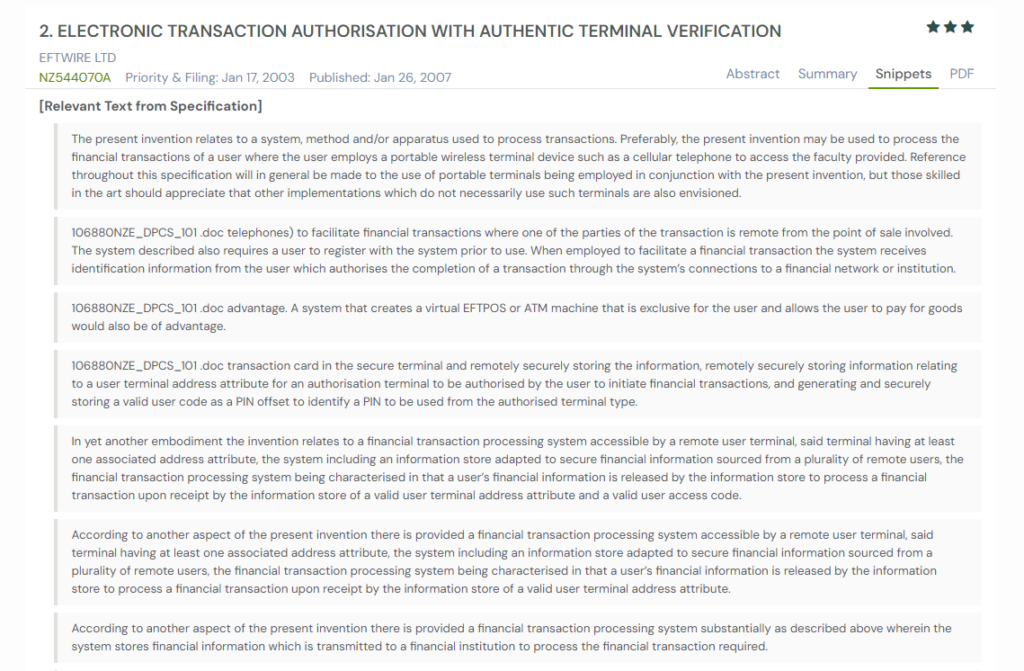

1. NZ544070A

This New Zealand patent, NZ544070A, published in 2007, outlines a remote financial transaction system using mobile terminals like cellphones. The system links users to virtual EFTPOS networks and uses terminal address attributes and access codes for authentication.

Below we have added snapshots from the GPS tool highlighting the relevant snippets from the specification for the similar patents.

What This Patent Introduces To The Landscape

- Remote EFTPOS transactions – Enables real-time point-of-sale payments via mobile devices from any location.

- Terminal address attribute authentication – Uses caller ID or device-specific routing addresses to verify terminal identity.

- Access code pairing – Combines user access codes with registered terminal IDs for dual-layer authentication.

- Virtual card mechanism – Simulates an EFTPOS card from a secure database, allowing card-free transactions.

- Encrypted communication payloads – All transaction data is encrypted before reaching the EFTPOS network.

- User registration without sharing bank data – Secure onboarding using token-based credentials rather than disclosing sensitive account info.

- Fraud detection and scoring engines – Monitors user activity to flag and prevent suspicious or unauthorized transactions.

- Support for multiple terminal types – Compatible with cellular phones, PDAs, landlines, and other remote access points.

How It Connects To US10032156B2

- Both systems allow secure financial transactions via mobile phones without modifying the SIM or hardware.

- Each relies on terminal-based user identification using attributes like phone numbers or SIM data.

- Both patents emphasize a central system that authenticates users and routes transactions securely to financial institutions.

- Registration involves mapping a mobile identity to financial access credentials without revealing sensitive account details.

- Each system enables remote banking and payment functionality outside of traditional point-of-sale setups.

Why This Matters

NZ544070A reinforces the viability of secure, mobile-initiated transactions without requiring specialized hardware. Its use of terminal address attributes mirrors the SIM-based verification in US10032156B2, making it a meaningful reference in discussions around mobile banking security and access control.

A similar verification workflow appears in US8209267B2, where the system automatically audits postage details and corrects any tariff mismatch to protect revenue.

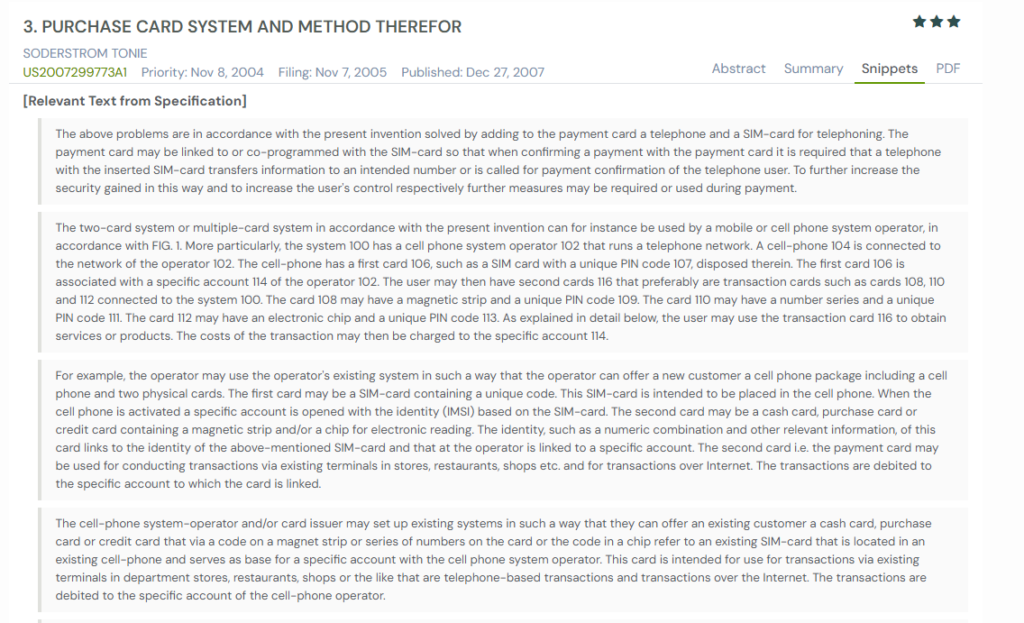

2. US2007299773A1

This US patent, US2007299773A1, published in 2007, describes a dual-card system linking a SIM-based mobile device with a payment card. Transactions are authorized only when the mobile device confirms the payment through the network using a verified PIN.

What This Patent Introduces To The Landscape

- Sim-linked payment authorization – Payment cards are linked to mobile SIM cards for secure transaction control.

- Dual-factor verification – In order to complete a transaction, the system requires both the physical payment card and mobile-based PIN entry.

- Real-time transaction feedback – Users receive immediate confirmation or rejection of transactions via their phones.

- Two-card integration model – Combines a SIM card and a separate transaction card under one verified account.

- Remote money transfers between users – Users can send funds to other subscribers within the same system.

- Cross-platform terminal support – Compatible with in-store, online, ATM, and remote internet-based payments.

- Automatic fraud protection – Transactions are blocked if PINs are not verified via the linked SIM device.

- Payment window feature – Limits transaction time, value, or location for added control and fraud resistance.

- Account balance visibility – Users can check available funds at any time through the mobile interface.

- Unified billing system – The system deducts all charges, including calls, data, and purchases, from the same account.

How It Connects To US10032156B2

- Both patents link a mobile device to a financial transaction system using a SIM-based identifier.

- Each system enables secure transactions without modifying user hardware.

- Both approaches ensure that the system authenticates users before processing requests.

- Each integrates mobile communication with financial services for seamless payment execution.

- The use of real-time PIN validation mirrors the SIM-based role confirmation in US10032156B2.

Why This Matters

US2007299773A1 demonstrates how mobile networks can serve as secure gateways for authorizing physical and digital transactions. The use of dual-device coordination enhances transaction security and reflects a growing trend toward integrated telecom-financial ecosystems.

Related Read: For additional perspectives on authentication beyond SIM and PIN methods, see our analysis of US9450956B1 and similar biometric key patents.

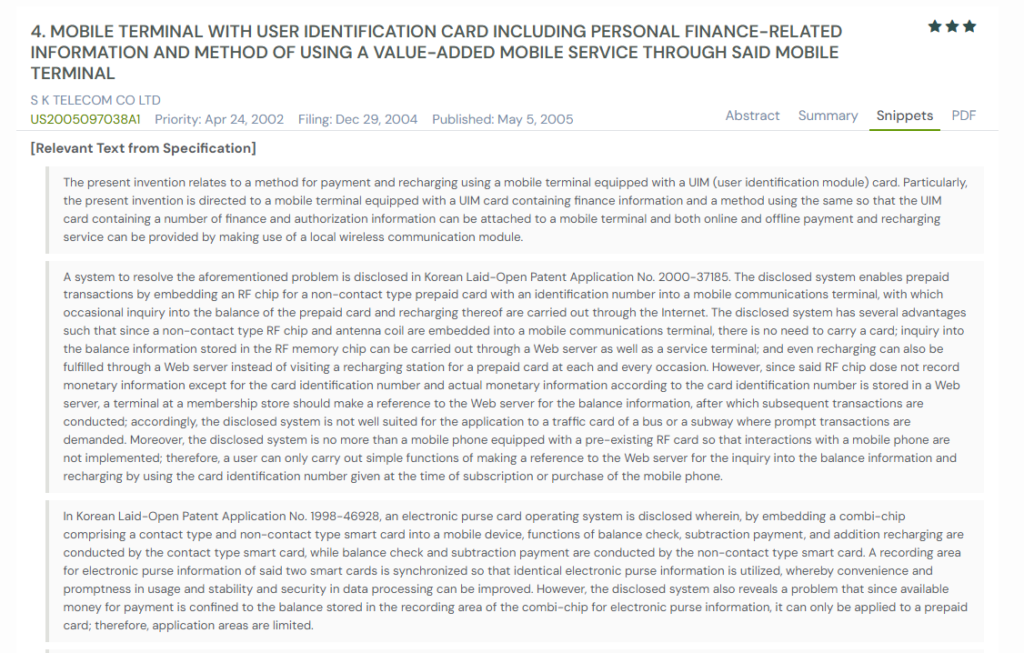

3. US2005097038A1

This US patent, US2005097038A1, published in 2005, describes a mobile terminal equipped with a user identification module (UIM) card containing personal, financial, and authorization data. It enables the user to perform payments, recharge prepaid cards, and access various value-added services through both the internet and local wireless communication.

What This Patent Introduces To The Landscape

- Finance-enabled UIM card integration – Combines mobile identification with credit, debit, and prepaid card information into a single removable UIM.

- Dual communication methods – Supports both internet-based and local area wireless payment processing (RF, IrDA, Bluetooth).

- Secure payment authentication – Uses PIN-based validation before granting access to sensitive financial or personal data.

- Modular service selection – Offers payment, transaction inquiry, ticketing, and recharging from a dynamic user menu.

- Prepaid card recharging – Allows balance top-ups via financial institution integration without third-party hardware.

- Integrated ticketing system – Enables ticket selection, payment, and delivery directly to the mobile terminal.

- Traffic card functionality – Emulates transit fare cards through embedded IC chips and RF antennas in battery packs.

- Roaming financial services – Users retain access to personal finance and identity services even when switching terminals.

- Data persistence in UIM memory – The UIM card stores all transactions for easy retrieval and sorting.

- Real-time balance and authorization – Direct communication with financial institutions ensures up-to-date transaction control.

How It Connects To US10032156B2

- Both patents focus on secure, mobile-based authentication for financial transactions.

- Each invention employs a user-specific hardware token (UIM or SIM) as a root of trust for enabling transactions.

- Both systems support multiple services (payments, inquiries, recharging) from a single mobile interface.

- Each enhances flexibility by decoupling financial credentials from fixed hardware terminals.

- The inventions emphasize real-time access to financial networks via mobile communication.

Why This Matters

This patent demonstrates a mature evolution of mobile terminals into full-service financial platforms. By embedding finance and authentication data directly into a portable UIM card, it creates a secure, multi-functional gateway that aligns closely with the future of mobile banking and identity verification across platforms and networks.

Mobile-only onboarding models like US8655341B2 rely on similar server-managed flows, where authentication, payments, and account creation are handled without requiring desktop interaction.

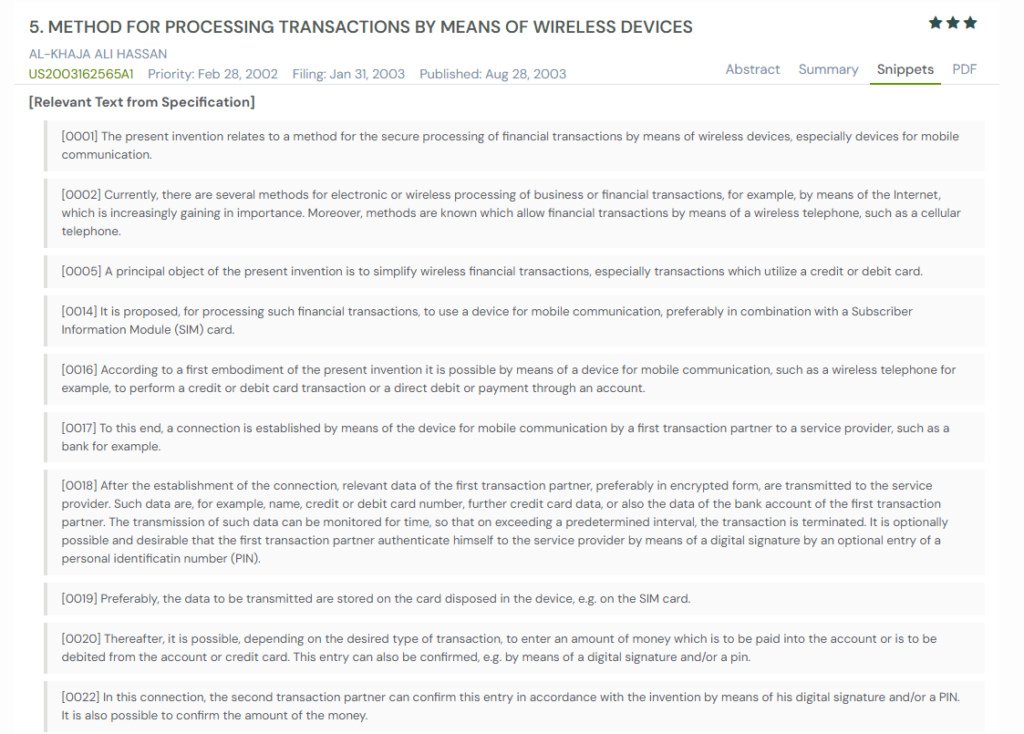

4. US2003162565A1

This US patent, US2003162565A1, published in 2003, introduces a method for processing financial transactions using wireless communication devices and SIM-based identification. The system supports dual-party authorization and encrypted data transfer, simplifying digital payments via mobile phones.

What This Patent Introduces To The Landscape

- SIM-based authentication – Uses SIM cards to store and transmit encrypted account and identity information.

- Dual-party transaction approval – Requires both sender and receiver to confirm with a PIN or digital signature.

- Time-bound transaction sessions – The system automatically terminates sessions if users do not enter data within a set time limit.

- Remote approval mechanism – One user can approve a transaction from a different mobile device.

- Pre-authorization feature – Enables advanced confirmation of spending limits or permissions by a second party.

- Unique transaction identifiers – Assigns a transaction or subscriber number to each financial exchange.

- PIN or signature confirmation – Every transaction step requires an explicit digital approval from the user.

- Data retention for retries – Users can retry failed confirmation attempts using stored requests or queued SMS.

- Cross-device flexibility – Users can confirm transactions from any compatible mobile device with proper credentials.

- Bank integration via mobile network – Direct connection to service providers like banks or card companies through the user’s mobile device.

How It Connects To US10032156B2

- Both systems enable secure mobile transactions using SIM-based user identification and encrypted communication.

- Each patent supports real-time PIN-based authentication before processing any transaction.

- Both solutions integrate with financial institutions without requiring hardware modification on the user device.

- The ability to link a mobile network to bank services is central to both technologies.

Why This Matters

This invention emphasizes dual-party control and flexible authorization, aligning well with current trends in secure mobile payments. Its focus on time-sensitive, identity-verified transactions supports a scalable mobile banking infrastructure where user authentication is paramount.

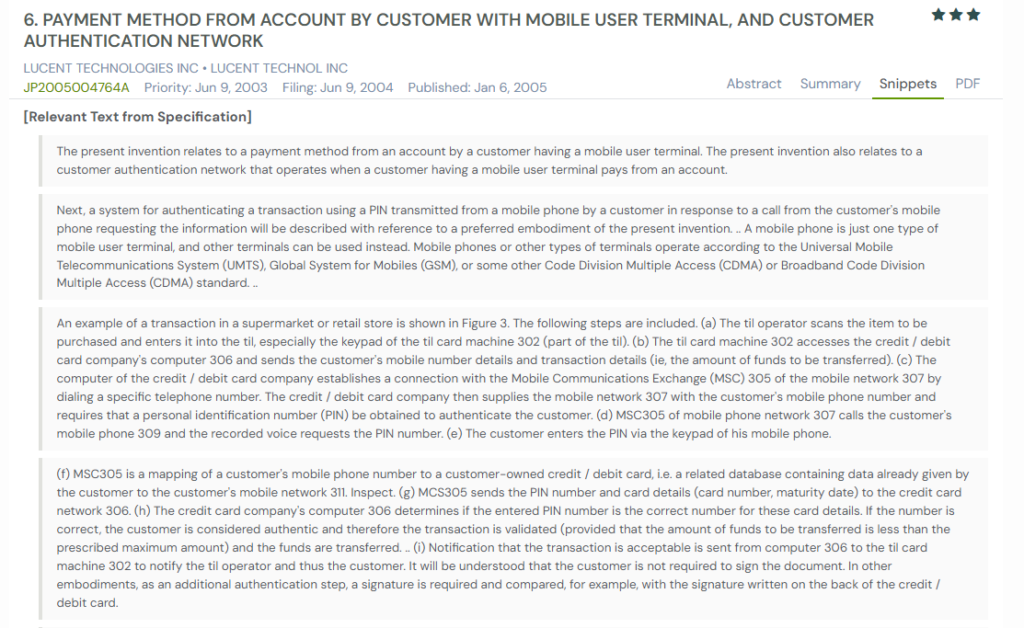

5. JP2005004764A

This Japanese patent, JP2005004764A, published in 2005, outlines a customer authentication system and mobile-based payment method using PIN verification. The system streamlines both in-store and online transactions by linking mobile terminals with card networks via secure authentication.

What This Patent Introduces To The Landscape

- Pin-based mobile verification – Uses a mobile phone to authenticate card-based transactions through PIN entry.

- Credit/debit network integration – Connects retail systems to card providers for real-time transaction processing.

- Automated mobile network handshake – Card providers initiate a call to the user’s phone to prompt for a PIN.

- Secure mapping of credentials – Links a user’s mobile number to specific credit or debit card details.

- Dual-channel transaction handling – Supports both physical retail terminals and online e-commerce platforms.

- Mobile network as verifier – Mobile infrastructure acts as a gateway to confirm user identity.

- Recorded voice prompts – Automated voice systems guide users as they initiate transactions.

- Real-time authentication loop – Verifies card and PIN instantly before confirming or rejecting payment.

- Multi-card compatibility – The system allows use with various card networks based on the selected PIN.

- No need for physical signature – Users approve transactions without providing physical verification, such as paper signatures.

How It Connects To US10032156B2

- Both systems enable financial transactions over mobile networks using SIM-based identification methods.

- Each relies on PIN-based user input for transaction verification and authorization.

- Both remove the need for physical modifications to mobile hardware or payment cards.

- Each connects users, mobile networks, and financial institutions in a streamlined digital loop.

Why This Matters

This invention highlights a flexible, multi-channel mobile payment system that aligns with modern authentication needs. It reflects the convergence of telecommunications and financial services, a key aspect shared with US10032156B2.

Related Read: US9549388B2 and similar patents show how hybrid navigation keeps services running seamlessly offline and online. Mobile payment verification patents tackle the same reliability challenge, anchoring secure approvals even in shifting network conditions.

How to Find Related Patents Using Global Patent Search

Understanding the broader patent landscape is essential when analyzing innovations in mobile-initiated financial transactions, SIM-based authentication, and dual-channel payment verification systems. The Global Patent Search tool simplifies this process by uncovering technologies that solve similar challenges around secure digital payment workflows and real-time user validation.

1. Enter the patent number into GPS: Start with US10032156B2. The GPS tool builds a focused query around this mobile-based transaction system. To narrow your results, refine the search with terms like “SIM PIN verification,” “remote card activation,” or “dual-authentication mobile payments.”

2. Explore conceptual snippets: Instead of analyzing claims line-by-line, GPS now offers curated text snippets. These highlight how other patents implement phone-based PIN prompts or second-factor confirmations through embedded secure elements in mobile devices.

3. Identify related inventions: The tool surfaces patents featuring SIM-integrated finance modules or methods for linking handheld devices to remote authentication servers. Many of these also address user experience factors like minimizing delays or supporting offline verification.

4. Compare workflows, not just claims: GPS emphasizes how each system handles secure user consent, authorization, or shared account access across mobile and card interfaces. This allows you to study parallel approaches, such as deferred authentication, PIN-over-voice prompts, or pre-authorized transaction frameworks.

5. Accelerate financial-tech insights: Whether you are in fintech, mobile payments, or authentication system design, GPS helps uncover inventive strategies that tie together device identity, user control, and fraud mitigation. From telecom-integrated validation to transaction routing, these insights reveal how real-world constraints are being solved creatively.

Related Read: To strengthen your research workflow, review our guide to the best patent analysis tools

With Global Patent Search, it becomes easier to trace how mobile terminals and user authentication protocols are shaping the next generation of secure, user-verified digital payments. Patents like US10032156B2 represent a growing trend toward integrated, user-controlled transaction systems that go beyond traditional card swipes or tap-to-pay models.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered legal advice. The related patent references mentioned are preliminary results from the Global Patent Search tool and do not guarantee legal significance. For a comprehensive related patent analysis, we recommend conducting a detailed search using GPS or consulting a patent attorney.